Every Successful Business Has Two Financial Loops

Today: Not many people pay attention to a business’s financial model, but it reveals a lot about their fate.

The Agenda 👇

The trading loop and the capitalist loop

You can find them in Vinci, McDonald’s, Amazon…

What if the two loops merge together?

Can you help me find The Family’s trading loop?

Every successful business has two different financial loops that feed one another:

One of them is a high frequency loop that generates a constant stream of free cash flow. It usually corresponds to what Fernand Braudel labels the “market economy”: you buy something at a price; you sell it at a slightly higher price; you pocket the difference (which can be enhanced by a negative cash conversion cycle). I call this the‘trading loop’.

The other loop, which has a lower frequency, usually corresponds to the capitalist part of the business: you insert capital into the production process for a long period of time, which in turn generates increasing returns to scale—that is, it increases the frequency and magnitude of the other loop, thus increasing the amount of free cash flow. It’s the ‘capitalist loop’.

It’s difficult for any company to make do with just one loop only. If a business venture is 100% within the market economy, money constantly flows in but it’s very difficult to scale up and generate increasing returns to scale. That’s typically what happens to a small business—it stays small because it focuses on mercantile trading rather than inserting the capital that would trigger increasing returns to scale.

On the other hand, if you’re 100% on the capitalist side, then you’re growing assets whose value compounds over time, with ever increasing returns on invested capital. But over the short term you don’t have free cash flow, which means you have trouble making a living. That is what happens to fund managers, which is why they negotiate with their LPs so as to be able to support themselves while the capital is working. Management fees are simply a cut of future returns paid in advance until the value of the assets under management comes to fruition.

The best approach for any business is to combine the two loops into a system, and make them fit together—that particular “fit” being a key component of a company’s strategic positioning. Indeed, it’s not about operating a trading business on one side and a capitalist business on the other. It’s much better than that: it usually consists in diverting a fraction of revenues derived from trading to insert them into the capitalist part of the system so as to generate those increasing returns to scale.

Over the long term, you might start realizing the compounded value on the capitalist side of the business, thus generating even more free cash flow and concluding that now you don’t need the trading loop. Yet some companies that have reached that stage still find it useful to continue trading:

As I already mentioned, you can still use those fast-paced recurring revenue streams derived from trading because, even if you don’t need them to cover the cost of operations anymore, you can invest them in new assets, thus strengthening the capitalist side of the business.

It enables data collection, thus keeping you sensitive to the market and strengthening your relationship with customers. This is why, for instance, Amazon continues selling goods directly, even if it (likely) doesn’t make a profit on them, rather than relying entirely on the marketplace or the revenue derived from it’s 20-year investment in AWS.

A third reason to keep the trading loop running even if the capitalist loop generates cash flow is to force your organization to remain gritty. It’s never a bad thing to keep the trader spirit alive and force everyone in the house to always be closing.

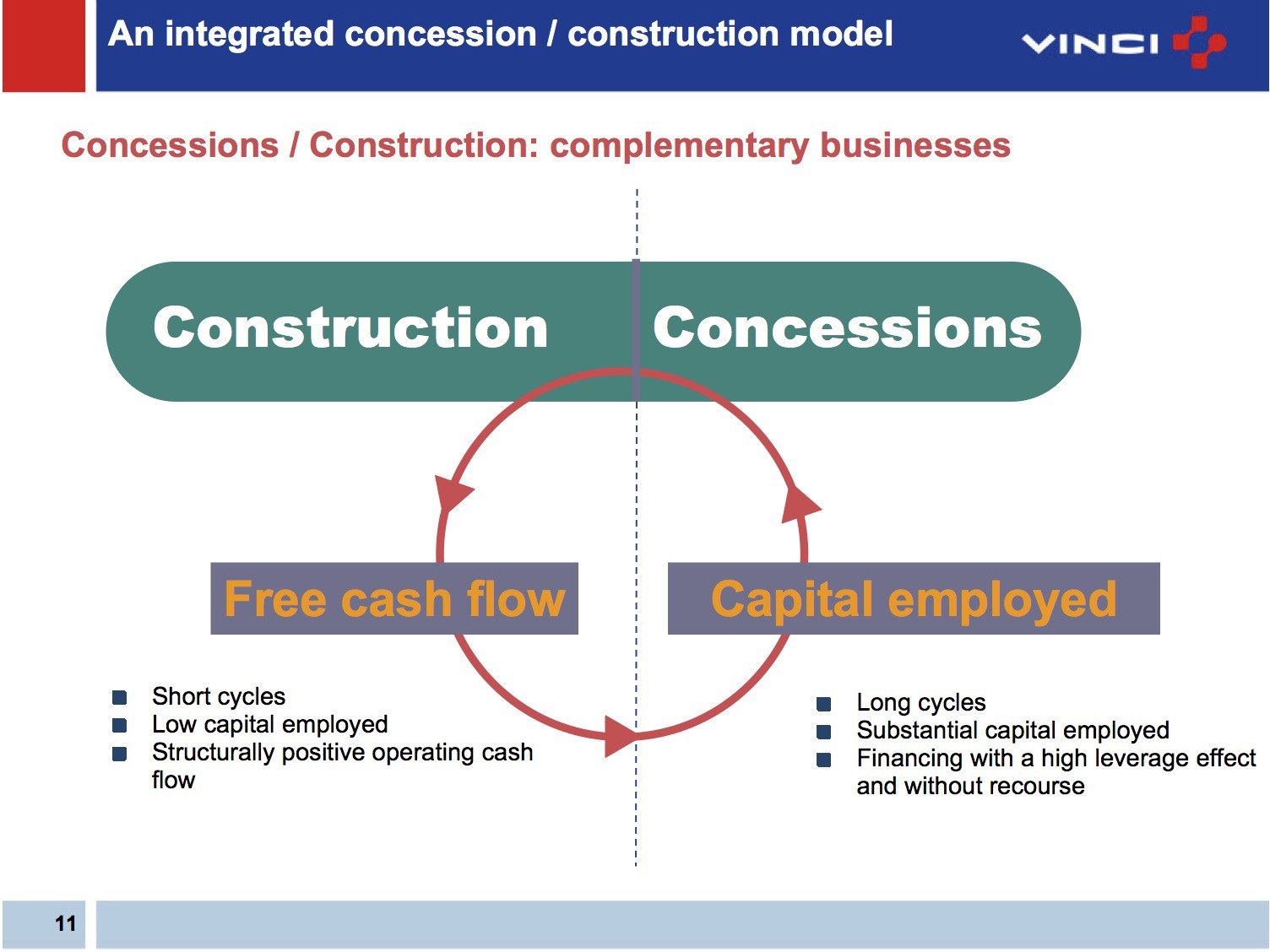

I first started to play with this notion of the two financial loops back in 2016 as I was studying the financial model of French conglomerate Vinci. Here’s what I wrote about it in my essay 11 Notes on Amazon:

Vinci’s dual business model has been designed for financial reasons. Construction is a low-margin business that employs little capital; but it generates massive amounts of free cash flow thanks to a negative cash conversion cycle (construction contractors take their time in paying their suppliers). On the other side of Vinci’s business model, utilities are very demanding in terms of investment and accordingly employ a lot of capital throughout very long investment cycles (sometimes decades); but in time they generate substantial net income that, ultimately, makes most of Vinci’s profits and dividends. All in all, the two businesses are complementary: without the construction business, it would be very difficult for Vinci to invest in its utility infrastructures, lest they bear the risk of excessive leverage; and without the concession business, Vinci would be incapable of turning substantial profits for its shareholders.

As you see, the trading loop is provided by the construction business and the capitalist loop results from operating concessions such as airports, highways, and others.

Since then it has become a framework for me: whenever I look at a business, I look for the two financial loops. If they exist, I know it’s a successful, self-sustaining business enjoying increasing returns to scale. If not, I know there’s only so much the business can do before reaching exhaustion.

Another example of combining the two financial loops is McDonald’s, which I wrote about in my Thoughts on Value Chains, and Why You Really Need To Get a 'Grip':

As explained by this great scene of the movie The Founder, Ray Kroc (the “founder”) had the brand and the ‘Speedee System’, but that didn’t translate into a capacity to expand faster: the brand was simply not valuable enough at the time. This is when Harry J. Sonneborn, who went on to become Kroc’s CFO, suggested buying land for two reasons that are well explained in the scene: you get ahold of assets that you can then use to raise capital (that’s increasing returns through the detour of raising more money); and you get a ‘grip’ over the franchisees, which makes it easier to keep them in line and retain most of the value added.

The trading loop, paradoxically, is about borrowing money from the bank with land as collateral. The capitalist loop is about collecting revenue from the franchisees operating restaurants on this land.

A third example is...any large retailer. You might think a retailer belongs to the market economy and barely has a capitalist component (hence, their difficulties scaling). But no: retailers invest a lot on the capitalist side (specifically in logistics) so as to increase capital velocity, as explained by Mary O’Sullivan:

The productive role of capital has resonance for the trade, wholesale and retail industry that has become an exemplar of the post-industrial economy in the US and elsewhere. Indeed, what distinguishes Wal-Mart, the industry giant in the United States, is its overwhelming commitment to “hard-driving” its capital compared with its competitors. As a result,it significantly outperforms its closest US competitor, Target, in the utilisation of both its fixed and working capital. If there is some “technological” logic that determines the relationship between the capital invested in the retail industry and the returns it ought to deliver, then Wal-Mart spends an inordinate amount of time in studiously neglecting it.

Amazon, of course, is no exception here. Like any other retailer, it combines a trading loop and a financial loop. Quoting my 2016 essay again:

Amazon, like Vinci, has a complex, pluralized business model that is tied together mostly by sophisticated financial engineering. There are many things that we don’t know, but we can guess about a great deal.

The absence of profit doesn’t mean that Amazon doesn’t generate cash flow. In fact, as Justin Fox wrote two years ago in the Harvard Business Review, “all that cash flowing in and sticking around a while before it has to go back out again makes it possible for the company to undertake experiments, learn from mistakes, and keep plowing ahead regardless of what those on the outside (such as shareholders) think.”

For instance, when it sells from its own inventory, Amazon doesn’t generate margins, but it surely does generate operating cash flow… and lots of data — because Amazon, not a third party, is the seller, it knows everything about both the customer and the transaction. That operating cash flow can then be allocated to capital expenditures, operating expenditures, and lowering the price of certain products. And all those allocation decisions are driven by the available data. One of the consequences is a better customer experience, which in turn generates higher liquidity on the marketplace where products are sold by third-party sellers. And on this marketplace, margins are higher for Amazon than when it sells from its own inventory, which secures the possibility for Amazon to generate net income in proportions high enough to reassure its shareholders.

All in all, without Amazon’s own inventory (and the cash flow it generates at the expense of suppliers), it would be very difficult to invest in and improve the customer experience, since they would constantly need to raise more cash; and without the marketplace, Amazon would be incapable of maintaining its profits and losses above the waterline. Amazon’s own retail business and the marketplace are loosely coupled, complementary businesses that enable sophisticated financial engineering dedicated to growth.

A fourth example is an investment bank. There are typically some parts of the business in which the bank acts as an agent, thus generating fees: that’s the trading loop. On another side of the business, the bank invests from its own balance sheet, thus nurturing the capitalist loop. Here’s the example of Goldman Sachs, as described by its then-CEO Lloyd Blankfein in a 2010 hearing in the US Senate:

Somewhere along the line, clients stopped asking necessarily to do things for them but to do things with them — in other words, to be the other side. And today in the world — and this evolved over a long period of time — to be effective for your clients, you not only had to give them advice, but you had to have the financial wherewithal — in other words, the balance sheet — to be able to accomplish their objective, not just advise them on their objectives. And so Goldman Sachs, 12 or 13 years ago, actually had to reverse many years of being a private partnership to become a public company so we could, frankly, survive in the evolving world of needing to be a principal to accomplish our client’s objective.

Just for the history of it, it was a very observed decision by the world and one that Goldman Sachs reached very reluctantly. The real rationale for it was not to make incremental profits; it was done in order for us to survive as a leading financial institution. Had we not done it, had we not grown, if we were not effective for our clients in order to allow them to accomplish those objectives, Goldman Sachs would be around, but it wouldn’t be an important company today.

A fifth example is Berkshire Hathaway, whose killer feature is that legendary “insurance float” that serves as permanent capital. The trading loop is made of all those insurance premiums, with the capitalist loop found in those dividends paid by the companies owned by Berkshire Hathaway. Here’s an excerpt from 11 Notes on Berkshire Hathaway, which I co-wrote in 2016 with my cofounder Oussama:

Thousands of articles are dedicated to better understanding Warren Buffett’s wise investment decisions. A lot less acknowledge the other side of Berkshire Hathaway’s business model, namely its very unusual way of financing investments with other people’s money obtained at a very low cost. Berkshire Hathaway has an unrivaled capacity to scale up, as opposed to more traditional models in the investing business, not only because Buffett and Munger reach better investment decisions, but also thanks to the unusual way they source the capital needed for those investments.

The secret that many miss when trying to devise Berkshire Hathaway’s success is how important its insurance business has been in the system and its dynamic. Without this insurance business and the extraordinary resources that it provided, Warren Buffett would have been unable to turn a failing New England textile company into an international conglomerate of remarkably profitable companies.

An insurance business makes a difference when you’re in the investing business because it generates formidable reserves that insurance company managers more or less invest as they see fit. It is those available insurance reserves that Berkshire Hathaway uses to finance its other businesses and make investments as large as the $5B Goldman Sachs investment in 2008 or the $28B Heinz acquisition in 2013. This “insurance float” has in effect proved the lifeblood that made Berkshire Hathaway’s extraordinary financial journey possible.

What happens when you become too good at this game? The frequencies of the two loops converge: assets have compounded so much on the capitalist side that they start generating free cash flow with the same frequency and magnitude as is seen on the trading side of the business. In this case, you don’t need much additional capital to be inserted into the company’s value chain, which results in two potential situations.

One option is to “commoditize the complement”, to quote Byrne Hobart: since you derive so much cash from the capitalist loop, you can unplug the trading loop by offering the related product at a lower price, or even for free—with scale, a powerful brand, and some network effects contributing to maximizing returns to scale. This is what has happened historically to equity research, as explained here by Marc Rubinstein: clients were paying for the research but at some point the banks decided to offer it “for free” because they made much more money on another side of the business.

Obviously, people have been taking note and realizing that there’s always a point when the free cash flow derived from the capitalist loop is enough to make the business grow. Therefore they’re ready to renounce the trading loop from the beginning, instead raising the corresponding amount of necessary capital on the market. This is what happens with all these tech businesses that start by offering a free product: they renounce a trading loop from the get go, and they count on the capitalist loop kicking in at a later point in time—with the costs between those two moments covered by venture capital.

The second option when the two loops converge is not cutting the price of the product and instead sending the money back to shareholders in the form of dividends or share buybacks. This is what the late Clayton Christensen was denouncing when he crafted the concept of a “capitalist’s dilemma”:

I.R.R. goes up when the time horizon is short. So instead of investing in empowering innovations that pay off in five to eight years, investors can find higher internal rates of return by investing exclusively in quick wins in sustaining and efficiency innovations.

I’m all the more interested in this topic of the two financial loops because my own firm, The Family, has to live with one loop and without the other. On one hand, we’re growing a portfolio of illiquid assets whose value compounds over time—shares in tech startups and carried interest on SPVs. On the other hand, we have always had difficulties generating a complementary loop on the trading side that would provide us with free cash flow to cover operating expenses and enable us to deploy more capital into our portfolio. In sum, we have a rather strong capitalist loop, but we suck at trading.

By the way, I already wrote about this in my A Memo About My Firm, The Family:

There are really two options for sustaining a financial model that brings together high returns and enough liquidity to get going. One approach is to get shares at the very beginning and then sell a fraction of a well-managed portfolio at a steady frequency so as to pay for the infrastructure along the way. Another is to raise funds and have them under management in exchange for a fee, then deploy them using pro-rata rights as has been the model of Y Combinator for a very long time (although they’ve announced they would stop following up in every deal from now on—a decision that was commented upon here).

From 2018 to earlier this year, our vision was that we needed to build up The Family’s equivalent of Berkshire Hathaway’s “insurance float” under the form of service businesses that would fit into our portfolio’s ecosystem. These companies could then contribute to funding operations at the group level via dividends or cash pooling. Alas we encountered two problems:

The first is a passing one, but still impactful: the pandemic and the resulting economic crisis has been very hard on these businesses, thus drying up our potential sources of free cash flow.

The other problem is structural: we haven’t found the“grip” yet for these service businesses, one that would be similar to what McDonald’s enjoys over its franchisees thanks to owning the land “upon which this burger is cooked”.

And so I would be curious to know what you think: do you know of comparable businesses that have solved this problem—growing a portfolio of holdings in early-stage tech startups while enjoying a trading loop that generates free cash flow on another side of the business?

If you’ve been forwarded this paid edition of European Straits, you should subscribe so as not to miss the next ones.

From Munich, Germany 🇩🇪

Nicolas