What High Interest Rates Do To Startups

European Straits #243

Hi, it's Nicolas. In this edition, I build upon geopolitical strategist Peter Zeihan's thoughts on innovation to investigate the present state of venture capital (VC) and startups. One crucial element that significantly influences their prospects is the macroeconomic context. Therefore, today I'll be addressing the question: How do interest rates affect startups?

1/ Innovation takes its most significant strides within financial bubbles. This phenomenon is, as often with innovation, attributed to uncertainty. When investors fund companies working with novel and poorly understood technologies, they face uncertainty from almost every direction. It’s impossible for them to predict the market's size, the venture's ultimate scale, the business model that the company will discover along the way, or whether it will be profitable.

In essence, investors grapple with as much, if not more, uncertainty than the founders they support. This is precisely why professional investors don't rely on a single company but instead diversify their investments across a portfolio. It's also why they seek to mitigate the pervasive uncertainty by exerting control over the companies they back and negotiating favorable terms to safeguard their invested capital. Board seats, liquidation preferences: those are all hedges against uncertainty.

Nonetheless, no adjustment can eliminate the uncertainty entirely, leaving investors to navigate much of their decision-making in obscurity. As a result, they cast their gaze in various directions, observing the actions of their peers, and often following the crowd. And then when this collective of near-blind investors, relying on each other for investment direction, swells in size and enthusiasm, that's precisely when a bubble begins to form and, eventually, collapses.

2/ The fact that innovation flourishes within bubbles doesn't imply that innovation vanishes once the bubble bursts. On the contrary, these bubbles are often referred to as "productive," borrowing Bill Janeway's words. The substantial influx of capital leads to the funding of numerous companies, assets, and infrastructures, some of which endure over time. In certain cases, these entities even contribute to a paradigm shift, ultimately changing the world.

Take Amazon, for example. Founded in 1994, it raised and spent about $3B before going public in 1997, a feat that wouldn’t have been possible if it weren’t for the dotcom bubble. Then when the bubble burst in 2000, Amazon could have faced demise had its then-CFO, the late Joy Covey, not secured financing on the bond market. This move allowed the company to evolve into the massive and transformative industry player it is today, both as a retailer and through its cloud service provider, AWS.

Let's examine another case: Google. Larry Page and Sergey Brin founded the company in 1998 on the Stanford University campus. In June 1999, less than a year before the Nasdaq experienced a downturn, Google secured a substantial $25 million investment from Kleiner Perkins and Sequoia Capital—a significant sum at the time. When the startup capital markets became less favorable from March 2000 onward, Google had a sufficient financial cushion to persevere. Eventually, it uncovered its successful business model through AdWords, evolving into the industry giant it remains today.

(In fact, Google did not seek any further funding from VC firms following its 1999 Series A round, and it went public in 2004. Their total funding as a private company amounted to just $26.1 million 😮)

This notion of bubbles funding numerous ventures, with a few leading to lasting and world-altering impacts, was well captured by economist Brad Delong in a 2003 Wired article, Profits of Doom:

Investors lost their money. We now get to use all their stuff. What got built wasn't profitable, but a large chunk of it will be very useful.

3/ Now, let's consider interest rates. Are low interest rates a prerequisite for the formation of a productive bubble like the dotcom one?

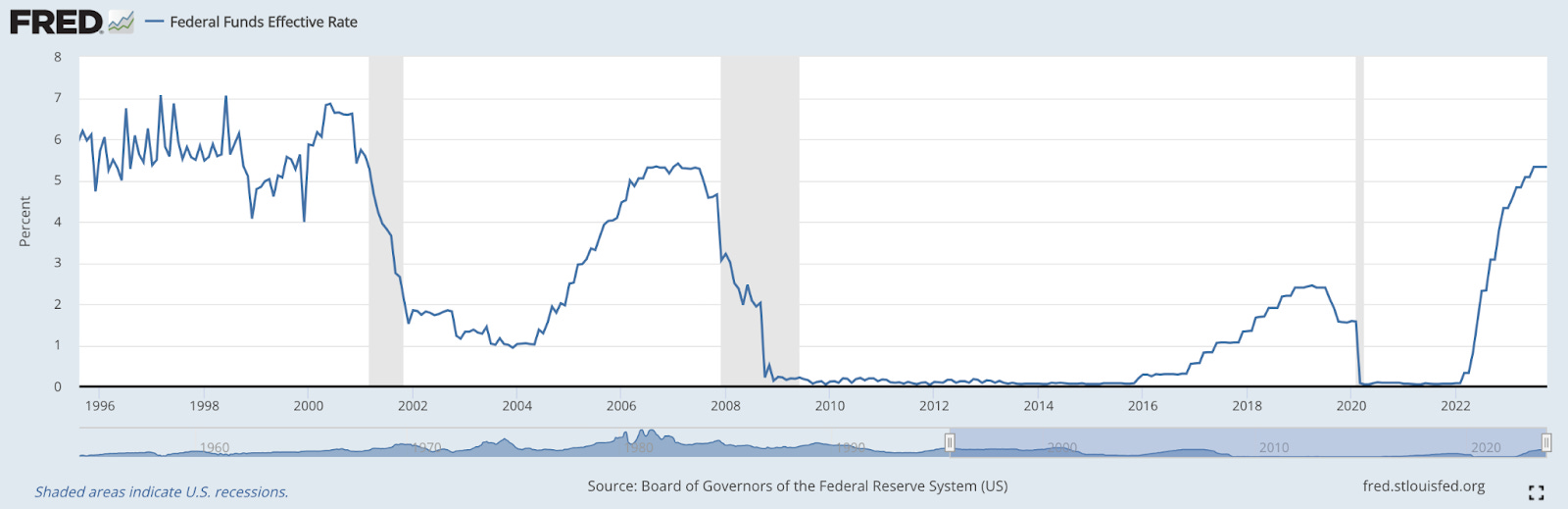

To answer this question, let's examine the historical evidence using this chart, which begins on the day of the Netscape IPO (August 9, 1995) and concludes as of a few days ago (October 2, 2023):

To me, it doesn't seem like the interest rates during the dotcom era were particularly low. In fact, they were higher on average than the purportedly high interest rates we are experiencing today—during a period marked by exceptionally high inflation and necessitating assertive action from central banks!

I have a vivid recollection of the dotcom era, when Alan Greenspan, the superstar central banker, held sway. During that time, many were urging him to increase interest rates due to the remarkably low unemployment rate, with concerns looming about the potential resurgence of inflation.

Sure, full employment often leads to wage demands, potentially triggering inflation. But Greenspan's argument during that period was that the combination of globalization and innovation acted as a potent counterforce against inflation. If workers could access less expensive goods from abroad and benefit from technology-driven cost reductions in services, they would be less inclined to seek higher wages. Consequently, interest rates could be maintained at a ‘low’ level without jeopardizing the overall macroeconomic equilibrium.

All in all, while the interest rates from the dotcom era may seem high from our 2023 perspective, the prevailing narrative back then was that Greenspan was taking daring steps by maintaining them at what was perceived as a perilously low level. This perception likely bolstered investor confidence, consequently playing a role in inflating the dotcom bubble.

4/ There's a crucial aspect to grasp about interest rates: it's not solely their absolute level at any specific moment; instead, it's the direction in which they are moving—whether upward or downward—and the related expectations that economic agents derive from the enigmatic language used by central bankers.

To illustrate this, let's recalibrate the chart above, shifting its starting point from the day of the Netscape IPO in 1995 to the day of the Shah's downfall in Iran (February 11, 1979). It provides a very different picture:

Dotcom-era investors likely viewed themselves as fortunate to operate during a period of relatively low interest rates, compared to the recent past. While the federal funds effective rate hovered around 5% during that time (which to us appears to be a high rate), the preceding decade, led by central banker Paul Volcker, experienced much higher rates, even reaching peaks of over 15% or 20%, depending on the timeframe.

Today, it seems like a 5% interest rate is high. When central banks set rates at this level, they signal a need for restraint. However, 5% isn't exceptionally high when compared to the 1979-2000 period. In fact, our current perception results from the exceptionally low rates experienced until 2022.

5/ Why have interest rates stayed so low for over two decades—with a brief exception in 2006-2007 when rates were higher than average over this period, but still comparable to the prosperous 1990s?

I'd attribute our prolonged low interest rates to two primary factors:

Frequent crises: We've experienced numerous crises that prompted central banks to lower interest rates to support national economies. A quick review of these shocks highlights the tumultuous macroeconomic landscape: it began with the dotcom crash in 2000, followed by 9/11 the following year, the 2003 invasion of Iraq, the Lehman Brothers collapse and the global financial crisis, the global pandemic, and the war in Ukraine.

Limited effectiveness of fiscal policy: Managing macroeconomic policy involves handling two levers simultaneously—monetary policy, which regulates the overall money supply, and fiscal policy, which dictates government spending as a % of GDP. During much of the 2000-2020 period, fiscal policy was notably inactive for various reasons, including ideological preferences such as the ill-advised austerity measures of 2010-2012, and institutional constraints on government spending, particularly within the EU and notably the Eurozone.

During the pandemic, fiscal policy regained momentum, with governments opting for substantial spending instead of relying solely on central banks to manage the front-line response. Predictably, this paved the way for central banks to once again contemplate raising interest rates—a move that was not only necessitated by the need to curb resurging inflation but also, perhaps, because central bankers felt relieved to no longer hold an exclusive role as stewards of the global macroeconomic landscape.

In an intriguing interview, financial researcher Russell Napier goes as far as suggesting that the global pandemic has shifted control over the money supply from central banks to governments:

My argument is that the power to control the creation of money has moved from central banks to governments. By issuing state guarantees on bank credit during the Covid crisis, governments have effectively taken over the levers to control the creation of money. Of course, the pushback to my prediction was that this was only a temporary emergency measure to combat the effects of the pandemic. But now we have another emergency, with the war in Ukraine and the energy crisis that comes with it… Governments won’t retreat from these policies.

6/ Low interest rates in the past two decades, especially post-global financial crisis, benefited startups and the VC firms backing them in two key ways:

They inflated a productive bubble, funding many ventures, some unproductive but others transformative. Notably, Tesla raised $19.4B, making electric vehicles mainstream, and OpenAI, which raised $11.3B (including from Microsoft) set off the Generative AI craze. In the context of the recent burst of the global pandemic bubble, these companies are akin to what Amazon and Google were during the dotcom era's bubble. It’s fair to say that they wouldn’t exist had it not been for the low interest rates of the past 15 years.

They allowed governments to borrow at low rates, enabling funding for pro-innovation policy. This, in turn, facilitated venture capital investments in startups. Notably, green tech efforts by some VC firms in the 2000s (see: Kleiner Perkins) faltered due to a lack of prior government investment. Conversely, current ambitious green tech goals are attainable as some governments have aggressively leveraged low interest rates to invest heavily in the field, ultimately building a new platform on which a new generation of VCs and startup founders can now “dance”.

However, not all governments have chosen to participate in this manner. While the US and China aggressively supported domestic green tech industries, many European countries adhered to moderation and austerity during this unique macroeconomic opportunity. This divergence will result in varying success rates for startups and lead to a lasting gap in macroeconomic output. European countries missed the chance to catch up while they could, potentially hindering their future development.

7/ With interest rates on the ascent once more (while they may not have reached the levels seen in the 1980s, the upward trend is what truly counts), it serves as a significant indicator to all economic participants that we are approaching a shift in the macroeconomic landscape. This holds true for VCs and startup founders, too.

Clearly, this doesn't imply that owning shares in tech startups or a limited partner interest in a VC fund has lost its value. There will undoubtedly be numerous accounts of startups flourishing against formidable challenges, along with the anticipation of VC funds yielding substantial returns for their limited partners in the coming years.

Nevertheless, the decreasing availability of capital, a consequence of rising interest rates, will lead those responsible for capital allocation to grow more conservative. As Blackstone’s Steve Schwarzman recently stated, “If you are living in a no-growth economy and somebody can give you 12, 13 per cent with almost no prospect of loss, that’s about the best thing you can do.”

Consequently, capital allocators considering VC funds and startups may be deterred by what they perceive (rightly so) as a sea of uncertainty. This aligns with the notion that VC is on the brink of transformation, initially explored in Startups: The Door Is Closing:

Some fund managers, committed to their VC ambitions, will opt to stick with the uncertainty. However, as a result they will face heightened challenges in (i) raising funds and (ii) once those funds are deployed, generating returns significant enough to remain competitive in a high-interest rate environment—if only to be able to attract the next round of funding!

Other (more opportunistic) fund managers may choose not to swim against the tide and may proclaim: “Allocators seek certainty, and I will provide it.” I bet this is precisely when investing in B2B SaaS startups will undergo a rebranding, shifting from VC to what will resemble private equity.

8/ Will less venture capital result in diminished innovation? Interestingly, not necessarily so!

During my research for this edition, I revisited this highly informative interview with Russell Napier (referenced above) titled The World Will Experience a Capex Boom. Allow me to summarize Napier’s argument below:

Both private and public sector debt levels have surged to unsustainable heights—much higher than in the post-WWII era. Given that debt levels are expressed as a percentage of GDP, one strategy to reduce this metric is to boost the nominal GDP growth rate, otherwise known as the sum of (i) real GDP and (ii) inflation. And since achieving substantial growth in real GDP is notoriously challenging, inflation presents the simplest and most efficient means of reducing private and public sector debt to a more manageable level.

The global pandemic allowed governments a unique chance to begin this change. When the economy slowed down, they had to step in to help businesses and people. Central banks couldn't lower interest rates much more, and this wouldn't have convinced banks to lend more money anyway, given the context. So, governments stepped up by promising to pay back the banks if borrowers couldn't. This way, they took control of increasing the amount of money in circulation. This eventually led to inflation, and central banks raising interest rates again.

Still, realizing they can influence capital allocation in the economy (something they were restrained from doing from 1979 onward), governments are now exerting their newfound power and taking active steps to tackle important challenges that matter to citizens—including the shift away from fossil fuels, the battle against climate change, the enhancement of national defense, the reduction of inequality, and the reduction of our reliance on China. Various reasons drive this shift, from national security and reshoring to promoting innovation and safeguarding employment. But overall, national governments are reasserting their control all over the world.

In typical circumstances, central banks would increase interest rates in the face of rising inflation, leading to higher bond yields. In turn, this would make it harder for governments to borrow money, crushing inflation and restoring stability in the process. However, when governments recognize that inflation can enable them to maintain spending while reducing debt, especially in the public sector, a likely scenario (as per Napier's perspective) is that governments will resort to financial repression: this involves implementing measures to restrict the movement of capital, compelling domestic capital owners to invest in low-yield government bonds and (directly or through the government)… in long-term, uncertain projects.

“Long-term, uncertain projects?” Does that sound familiar? That's precisely my point. While rising interest rates may appear detrimental to VC and startups in the short term, another funding source could step in. Governments may compel domestic investors to allocate more funds (again, directly or indirectly) to ventures and financial products with uncertain returns but aligned with long-term, widely endorsed development objectives. It may not exactly resemble today's startups, but it can play a role in supporting our collective innovation endeavors, particularly if governments implement it effectively (which I will explore in a future edition).

9/ If we broaden our definition of startups to include those backed, either directly or indirectly, by national governments or investors tamed by financial repression, a recurring pattern emerges: there's a means of supporting such startups in nearly any macroeconomic context:

During periods like the dotcom bubble, a thriving ecosystem of private sector entities, including VCs eager for returns and innovation-driven founders, needs to be present and leverage the speculative bubble's growth to build companies like Amazon, Google, Tesla, and OpenAI.

When the productive bubble inevitably bursts or unexpected shocks like the 2008 global financial crisis or the 2020 global pandemic occur, the resulting policy mix, characterized by low interest rates, signals to governments that it's time to borrow freely and allocate more funds to upstream scientific research and other innovation-oriented public spending areas. These investments, in turn, facilitate private-sector led innovation when economic growth resumes.

Finally, in cases where interest rates have remained low for an extended period, and the debt level becomes unsustainable, as is the case today, governments may take direct intervention measures to manage the economy, potentially funding innovative ventures through financial repression.

What stands out when reviewing these three very different regimes is how the US has effectively supported startups and innovation over every period, irrespective of interest rates. The US maximized the potential of multiple productive bubbles since 1995, followed by significant public spending to create a platform for future innovators. Presently, there are indications of direct government intervention under a new industrial policy, aimed at fostering innovation for long-term objectives such as addressing climate change, reducing trade dependence on China, and transitioning away from fossil fuels. As if the US innovation engine can never be stopped!

Indeed, the ability to innovate under any macroeconomic circumstances should be the goal for every country and its government. I will explore this topic further in upcoming editions. Feel free to share your thoughts 👇

10/ Below, you'll find a list of articles that I either read thoroughly or briefly skimmed while preparing this edition, along with a few written by myself:

Profits of Doom (Brad Delong, Wired, April 2003)

Insight: How cleantech tarnished Kleiner and VC star John Doerr (Sarah McBride, Nichola Groom, Reuters, January 2013)

The Austerity Delusion: Why a Bad Idea Won Over the West (Mark Blyth, Foreign Affairs, May 2013)

A History of Fed Leaders and Interest Rates (Pradnya Joshi and Binyamin Appelbaum, The New York Times, December 2015)

Better Get Used To Those Bubbles (me, Medium, March 2016)

The ‘Pas de Deux’ of the State and Venture Capital (me, Medium, March 2019)

Inflection Point (Marc Rubinstein, Degrees of Certainty, August 2019)

How Monopolies Broke the Federal Reserve (Matt Stoller, The BIG Newsletter, August 2019)

The World Has Gone Mad and the System Is Broken (Ray Dalio, LinkedIn, November 2019)

This is how much harder it is to raise capital during a downturn (Collin West, Nihar Neelakanti, and Gopinath Sundaramurthy, Kauffman Fellows, March 2020)

Are you prepared for Financial Armageddon? (Pär-Jörgen Pärson, Northzone, October 2020)

Why Is It Still So Hard to Raise in a Time of Cheap Capital? (me, European Straits, November 2020)

Larry Summers: ‘I’m concerned that what is being done is substantially excessive’ (Martin Wolf, The Financial Times, April 2021)

Productive Bubbles (Bill Janeway, NOEMA, July 2021)

Were Alan Greenspan Ever to Let His Hair Down… (Brad Delong, Brad Delong’s Grasping Reality, November 2021)

Edward Chancellor: Central banks delayed the day of reckoning (Mark Dittli, The Market, July 2022)

Russell Napier: The world will experience a capex boom (Mark Dittli, The Market, October 2022)

What Drives Innovation? (Bill Janeway, Project Syndicate, January 2023)

The new industrial policy, explained (Noah Smith, Noahpinion, May 2023)

Private equity firms pivot away from traditional buyouts (Will Louch, The Financial Times, September 2023)

What are bond yields and why are they at a 25-year high in UK? (Richard Partington, The Guardian, October 2023)

Sign up to European Straits if you don’t want to miss the next issues 🤗

From Munich, Germany 🇩🇪

Nicolas